I remember in the 1970s, as sales manager for a startup New England natural foods wholesale distributor, receiving a $15,000 opening order blank check from an aspiring retailer. To my embarrassment, I couldn’t find—nor could I in good conscience recommend—enough top-selling items to fill the order. In those days, and continuing pretty much through the end of the millennium, it was the independent natural products retail channel, accessed primarily through wholesale natural foods distributors, that was the first, necessary, stop for new natural brands pursuing the emerging natural foods consumer.

Fast forward to today, where, at the major trade shows, in answer to the question, “Are you in distribution?” new natural brands exhibiting are just as likely to answer, “Yes, we’re in Costco,”—as in direct—as they are to say they’re listed with a wholesale distributor serving the independent natural products retail channel.

Challenge #1 – Product Strategy

Yesterday, independents had first crack at new brands entering the natural organic space. Today, new brands may bypass the independent retail channel altogether. If we are honest with ourselves, this shift away from independents toward more mainstream, mass market channels is clear proof the natural foods movement has succeeded. But it still leaves independent natural retailers in search of a product strategy.First Decision: Perishables or not?American consumers increasingly equate “fresh” with “quality,” and think of dry, packaged groceries as lower quality. This is why independents that devote little space to perishables are seeing a decline in their food sales.

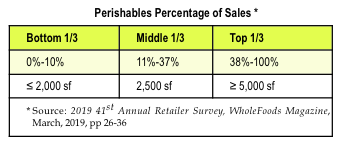

As our annual retailer survey shows each March, independent natural products retailers vary widely in the amount of fresh foods they sell. The one-third at the bottom carry 10% or less fresh foods, focusing instead on supplements, vitamins and personal care, and typically operate in no more than 2,000 square feet gross lease area (GLA). Those in the top third get at least 38% of their sales from fresh perishables, and operate in 5,000 to 10,000 square feet GLA, or more.

But it is the one-third of retailers in the middle, who sell more than a little—but not quite enough—fresh foods to convince shoppers to shop them daily, or at least weekly. These retailers operate in about 2,500 square feet GLA on average, which is not enough room for a full-perishables presentation, but is more than enough to display supplements and personal care.

Small stores of up to 2,000 square feet that focus on supplements and personal care can be profitable and easy to operate. But if your vision includes perishables, you should plan on making at least 40% of your assortment fresh foods, including some prepared on-site available for grab-and-go. The special equipment for cooking, preparation, and merchandising requires extra space to operate efficiently and to display properly. Trying to save money by keeping your total footprint small while cramming in these fresh departments is counterproductive. As we see fromWholeFoods Magazine’s annual survey,stores that focus on perishables in a larger footprint are able to unlock the increased traffic and higher sales these free-breathing fresh departments bring.

Small stores of up to 2,000 square feet that focus on supplements and personal care can be profitable and easy to operate. But if your vision includes perishables, you should plan on making at least 40% of your assortment fresh foods, including some prepared on-site available for grab-and-go. The special equipment for cooking, preparation, and merchandising requires extra space to operate efficiently and to display properly. Trying to save money by keeping your total footprint small while cramming in these fresh departments is counterproductive. As we see fromWholeFoods Magazine’s annual survey,stores that focus on perishables in a larger footprint are able to unlock the increased traffic and higher sales these free-breathing fresh departments bring.Second Decision: Product assortment and private labelWith supermarket, mass market, and club channels offering many of the same natural organic items—at better prices than you—sourcing unique products is critical for independents. As brands grow from launch to maturity, there is a natural progression from smaller distribution channels to larger ones. Some brands may be content to stay within the independent channel their entire lives, but for many, the ultimate goal is wider distribution.

You must be ready to let these maturing companies go when you no longer enjoy exclusive distribution. The good news is, there are hundreds of brands launching all the time. You only need a few good ones to create excitement and incremental sales in your store. But whatever you do, don’t make the mistake of trying to match prices with your deep-pocket competitors on identical items.

One way to ensure brand loyalty is to develop your own private label. There are several high-quality private label vitamin and supplement suppliers ready to provide basic and complex formulations geared to the independent natural products retailer, with reasonable minimum-order requirements. According toWholeFoodsMagazine’s 2019 retailer survey, about 30% of independents have a private label supplement line, with an average of 114 stock-keeping units (SKUs), a trend which has been growing each year.

If you are concerned about making the leap to private label, just remember that it is the go-to strategy for many of the largest retailers including Aldi, Costco, Kroger, Target, Walmart, and Whole Foods Market. In addition to locking in loyalty, shoppers can’t showroom your formulas to compare prices at your competitors, making private label one of your best long-term strategies for survivability and differentiation.

Third Decision: Online delivery and pick-upIt seems every major retailer is jumping on the “omnichannel” bandwagon, promising to provide products to customers anywhere, anytime. The trend is being driven by Amazon, which at the moment continues to enjoy the luxury of not having to prove delivering online orders the same day, sometimes within two hours, is profitable (educated guess: it isn’t), or having to demonstrate that flooding its Whole Foods Market stores with online order pickers isn’t disrupting regular shoppers (it is).

Are Amazon’s same-day and two-hour deliveries profitable? Educated guess: no.The short answer here is, if you don’t have a robust prepared foods program, you don’t need to provide delivery for online orders, or to fulfill online orders for pickup in-store. No one needs pickled daikon or aromatherapy candles shuttled to their doorstep in two hours, or ready for them to pick up in your parking lot.

Most independent retailers have difficulty making a profit from their prepared foods programs even without adding delivery. But if you are considering delivering your prepared foods, be prepared to lose money. Whether you pay your employees, or hire a third-party service, the costs will likely absorb all your profit, and may even cost you money.

If you do use a third-party service, you’ll be outsourcing your customer service standards to some gig-economy contract worker that does not have any loyalty to your brand. A recent survey of contract delivery workers revealed that 28% nibble the foods they should be delivering. I guess they’re hungry.

Fourth Decision: E-commerceOne of the worst decisions an independent natural products bricks-and-mortar retailer can make is to sell products online. Whether you use a product catalog from third-party fulfillment service, provide the products yourself, or to a third-party e-commerce platform, you will be working on very small gross margins. And without ponying up big dollars to raise your search results, you have no chance of competing with the native online businesses that specialize in internet sales.

It is not only the cash costs for fulfillment services, advertising and other fees, but the non-cash costs of managing the business. Do you really want to be distracted dealing with an online effort that has zero in common with your primary, bricks-and-mortar store? Every moment you spend handling online duties is a moment you are away from servicing your customers, managing your employees, and taking care of your store.

Challenge #2 – People Strategy

The folks that started the natural products movement wanted an alternative to mass-produced, highly processed foods. Newly inspired natural entrepreneurs enthusiastically educated their customers, one at a time, about the benefits of whole, less-processed foods, closer to nature. By telling and retelling the story of natural foods, independents inadvertently created a business model that elevated and intensified relationships, developing a deep, personal trust between each individual customer and storekeeper.Big box merchant Target has improved results by giving employees “ownership” of their departments. Turns out knowledgeable employees that engage with customers increase sales.First Decision: Customer-intimate, or not?The customer-intimate model is unique to the independent channel. In none of the other retail channels do employees get to engage the customer in a conversation providing personalized health advice. Of course, you train your employees to observe legal limitations, but for large supermarket, mass market, and supernatural chains, the risk of running afoul of laws that forbid diagnosing or treating disease is too great a legal liability to allow them that freedom.

By default then, the one-on-one customer education model remains the exclusive domain of the independent retailer, and one of the most powerful advantages over all other retail channels. Although the internet has unleashed the phenomenon of showrooming, with instant online price discovery, independent retailers would defeat themselves by withdrawing from the customer-intimate model that built the business, and that still differentiates it today.

Second Decision: CompensationThe recent multi-state trend to legislate increases in the minimum wage did not magically make all those on the bottom rung of the pay ladder more productive. But, if you are following the independent natural products retailer playbook by hiring knowledgeable employees, you have to pay better than the rest of the retail world anyway for front line talent that can sell.

Remember, retaining good employees, even if you have to pay them a bit more, is less costly than turning staff over frequently. The opportunity cost of lost sales while you search, recruit, hire and train the next employee easily exceeds the premium you pay to retain good help.

Be generous with your employee product discounts as well. Using a 25% discount off of regular retail should allow you to retain enough gross margin to offset your handling and bookkeeping costs. It also will discourage the corrupting influence of the five-finger discount employees may feel entitled to if you are stingy with discounts.

Paying employees to learn, and for professional development, also makes sense. At the least, you should put workers on the clock when they are studying educational materials you or your vendors provide. For employees wanting to gain nutritional expertise, subsidizing outside learning by offsetting some of these costs will promote loyalty to you and your store. One of the main reasons employees stay is the belief that they are gaining skills and adding responsibilities over time.

Challenge #3 – Place Strategy

We’ve talked about two of the three “Ps”: Product and People. But the three-legged stool bricks-and-mortar retailers need for a solid foundation includes what goes on inside the bricks: the Place where your customers shop. We hear a lot about how younger generations are willing to spend freely on “experiences.” What does this mean?Take a look at the music industry. Record and CD sales have been declining, while streaming services are increasing. Artists have had to look outside recorded music to make the money they once made in the recording studio, and have taken to the road to do live performance.

Taylor Swift’s tours will bring in $258 million this year, the highest in the industry. Hundreds of musical acts are touring for dollars, adding value to performances by offering schwag—the promotional products they “give” away in exchange for charging premium ticket prices. Tour promoters have gotten smart by mining big data to identify and stay in touch with fans, inviting them to shows, adding special perks like preferred seating and other incentives. All of this adds up to a premium “experience” for the fans.

Shopping malls have adopted a similar strategy, introducing live performance, adding events and activities, and tying it all together with enhanced food and dining experiences.

Retailers in New York City’s Times Square are also adding activities, and department stores are leasing space to high-end restaurants that act as a separate draw to bring customers in. They hope customers coming in for the food experience will stay and shop, if not this time, then soon, and that they will tell their friends about the experience.

The first step in creating an “experience” for shoppers is up-to-date equipment, lighting, and fixtures.First decision: Spending the moneyAll of these examples of experiences have a common thread: significant investment. Any one of these approaches to enhancing the shopping experience requires spending money. To increase your space for prepared and perishables foods, or to upgrade to more attractive lighting, flooring, equipment and fixtures that entice customers to linger longer, learn and spend, you are going to have to invest.

During the first 30 years of the natural foods movement, independent retailers grew organically because they held an exclusive on the products. Almost without thinking, independents chalked up yearly growth without having to reinvest in their physical space beyond their initial build-out costs. But this is an anomaly in the world of retailing.

Every retailer, regardless of the product or service they offer, must refresh the presentation on a regular cycle. Refrigeration equipment wears out, and new cooling and lighting technology is more efficient and beautiful. Flooring surfaces wear out, and new materials mimic the look of wood, but with better durability. If you don’t invest in your presentation, your store will look shabby compared to your competitors that do.

Are you part of the future?

Recent survey data is promising. Gen Z, those born after 1996, the oldest of which is now 23, reports they want and plan to shop in bricks-and-mortar stores at Christmas. Unlike their older brothers and sisters in the millennial generation, Gen Z is not in awe of smartphone technology. The basic human need for face-to-face interaction and real, live relationships is reasserting itself, and manifesting in our youngest people.Millennials are entering their 40s, and beginning to feel the first signs of aging. Fortunately, their earning power is also increasing, enabling them for the first time to afford the natural remedies on your shelves.

Both these generations, millennials and Gen Z, will drive the next phase of growth for the natural products industry. They are aligned with our values of sustainability and transparency. The question is, are you willing to do what it takes to create a destination that will attract them, giving them reason enough to choose you as opposed to your competitors? The choice is yours. Your opportunity awaits.WF