The natural skincare market has undergone a dramatic change since 2005. What was once a niche market offered predominately through Natural Retailers and Spas has emerged into the mainstream consciousness and conventional distribution channels. Industry reports state that the natural skincare market continues to grow exponentially, from $3.3 billion in 2005 to $5.9 billion by 2011, and is projected to reach $9.3 billion within the next year (1).

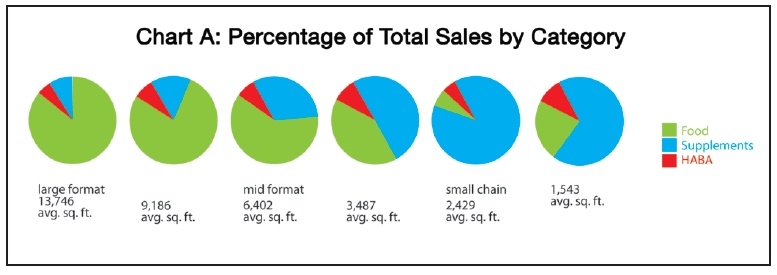

Due to the high price point and handsome margins of 50–60%, the premium natural skincare category is positioned to offer significantly higher revenue than most categories for independent Natural Retailers. However according to the 2013 WholeFoods Magazine Retailer Survey (2), on average the HABA category only contributes 6.2% of revenue. Even across the wide variety of independent Natural Retailers, with major differences in their offerings, the contributions by the HABA category is consistently low (see Chart A).

With such substantial category growth, one would expect Natural Retailers to be enjoying a great surge in profits over these past eight years. And while some Natural Retailers’ HABA sections are excelling, 2012 discussions with a national natural retail chain and multiple independent Natural Retailers suggest quite the contrary, and even show that many retailers are challenged, in fact, to sustain a robust HABA section. According to Jay Jacobowitz, founder and president of Retail Insights, “There has not been much movement in the HABA numbers for decades; a range of mid-to-upper single digits (5–8%).” Getting customers into aisles and purchasing the premium offerings proves to be an ongoing challenge.

Natural Confusion

Few categories enjoy skincare’s level of shopper involvement and consideration; vanity is a very powerful motivator that can take precedence over comfort, health and well-being. By promoting the allure of the “ideal beauty,” the beauty industry perpetuates insecurity and uncertainty to sustain continuous demand and reliance on referrals at the point of purchase.

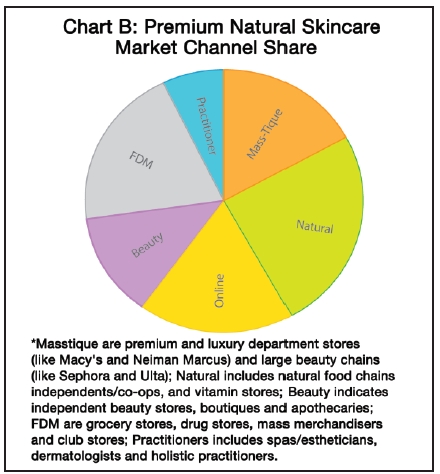

A multitude of highly sophisticated boutique brands from major consumer packaged goods manufacturers and beauty houses have gained access to the natural skincare market by promoting the “efficacy of the exotic.” While many of these brands are perceived as natural, many are not, which is an example of how perception fed by the desire for results dominates the skincare market. Much of the category growth has been realized under this auspice in conventional channels: masstique (i.e., premium & luxury department stores, large beauty chains), beauty boutique, online, drug and mass (see Chart B).

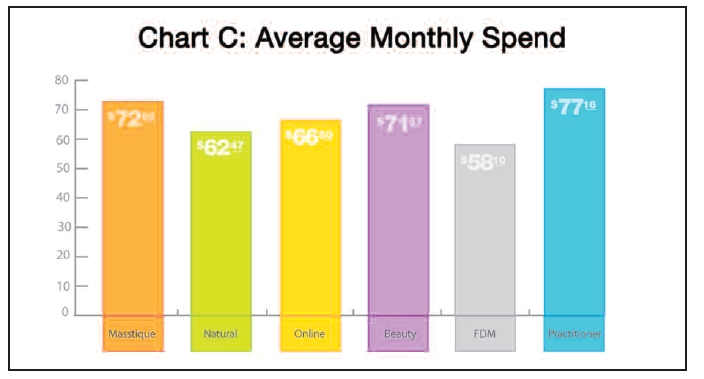

The resulting confusion within the natural skincare category is eroding the ability for effective differentiation among Natural Retailers and less sophisticated brands offered in the natural channel. Price stratification is a perfect example of this, where the natural channel appears to have a price ceiling compared to most other channels limiting the potential for dollar share and the robust margins associated with premium offerings (see Chart C).

Understanding Premium Natural Skincare

The Premium Natural Skincare Channel Dynamics study (fielded by Brand Reason to understand the current market atmosphere) examines natural skincare purchase dynamics across channels and how Natural Retailers can leverage their unique attributes to establish a competitive advantage. The study included three distinct consumer groups consisting of 952 premium natural skincare consumers representing the dominant category channels: natural retail, department, beauty, FDM (i.e., food, drug and mass channels), online and practitioner. Respondents answered 50 questions that provided insight into their demographics, attitudes and beliefs, skincare regimens, product preferences, skin conditions, health, loyalty, trust, motivations and purchase drivers and cross-category correlations within the natural market.

A key finding was that, like other categories of high concern where much consideration goes into each purchase, natural skincare participation is dependent on accessibility, social factors and the need-state impact on the consumer’s life.

A review of market demographics  reveals a direct correlation between the higher socio-economic strata, the availability of resources to maintain one’s looks and an increased focus on beauty. While the average natural products consumer tends to skew toward the upper socio-economic strata, the higher income consumers are spending much of their skincare regimen dollars in channels other than Natural Retail.

reveals a direct correlation between the higher socio-economic strata, the availability of resources to maintain one’s looks and an increased focus on beauty. While the average natural products consumer tends to skew toward the upper socio-economic strata, the higher income consumers are spending much of their skincare regimen dollars in channels other than Natural Retail.

In the oral care business, we know if people are not already brushing their teeth, we probably cannot get them to start. The business objective for Natural Retailers in the skincare market should be approached the same way, with a lesser focus on growing the category and a greater intent to capture a larger share from channels with strong behavioral correlations. Natural Retailers can leverage their equity and the strength of their customer relationships with these shoppers.

Product Targets for Natural Retailers

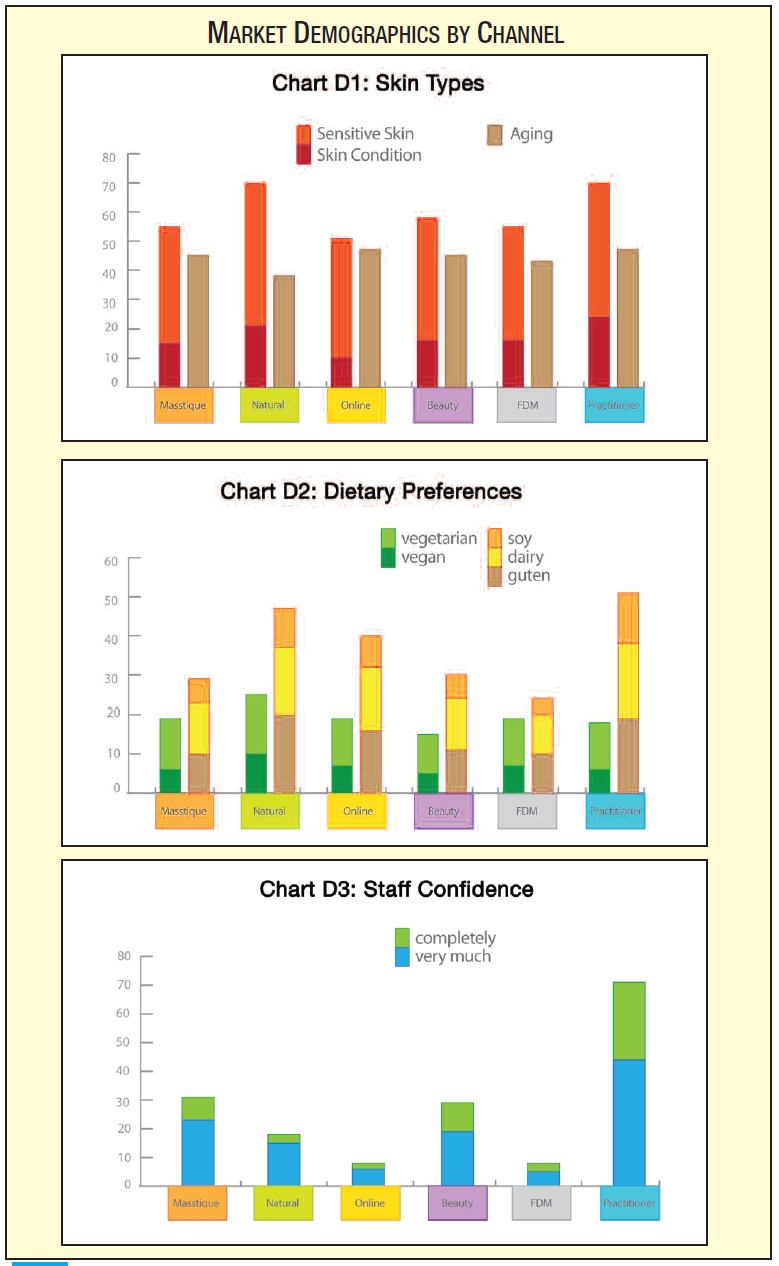

A cross-channel assessment of baseline variables such as product attributes and skin types reveals a moderate degree of differentiation across the market (see Charts D1–3). The dominant skin type is combination, followed by aging. A standout variable in both the Natural and Practitioner channels is the high occurrence of sensitive skin combined with having a skin condition (see Chart D1). Delving further into lifestyle factors suggests dietary preferences (avoidance diet) and supplement use (addressing a specific condition), which may indicate an even greater correlation between the two channels (see Chart D2). However, the Practitioner channel (comprising estheticians, holistic practitioners and dermatologists) enjoys a much higher level of consumer confidence than Natural Retailers; only the FDM and online channels—both unsupported sale channels—have lower confidence indices for staff referrals (see Chart D3).

The staff referral confidence index represents the critical need for Natural Retailers to increase their authority to establish relevance and consideration that drives demand and the premium price proposition in skincare. This is not to suggest that all HABA staff need to be better trained. Rather, the dialogue must change so that customers feel Natural Retailers understand their needs and are truly addressing what they desire.

Unlike other channels, the top purchase driver of Natural Retail customers is avoidance, a likely reflection of what the channel has consistently promoted (e.g., chemical-free, additive-free, gluten-free). This messaging has created a self-fulfilling prophecy for what customers have come to expect.

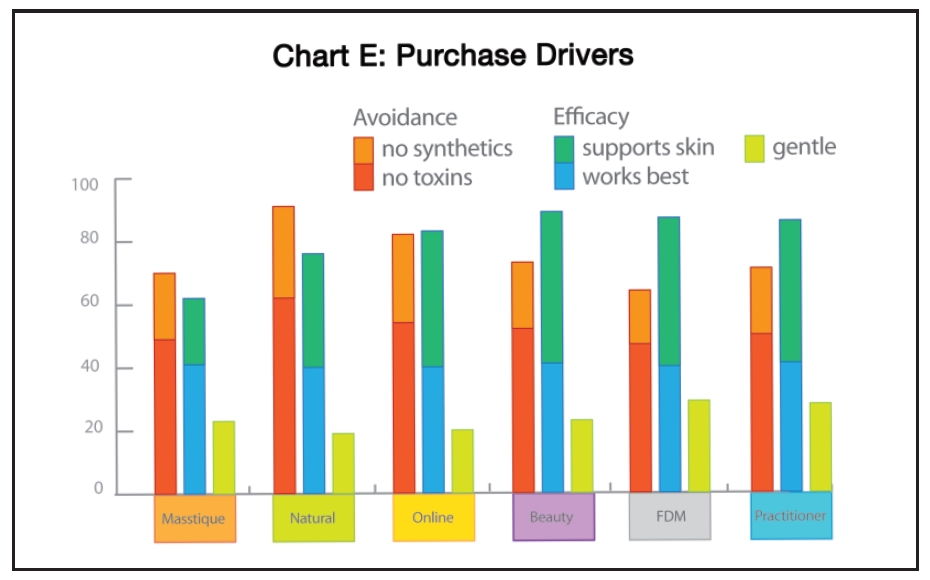

Industry has promoted claims of 100% pure, toxin and synthetic free, organic, for sensitive skin and gentle, which are requirements for customers seeking safe offerings that won’t cause irritation or worsen their skin problems. The channels with strong correlations to the natural channel (e.g., practitioner, beauty boutique, online and mass-tique) all benefit from more spending per customer and put a greater emphasis on efficacy (i.e., solutions for their skin problems), suggesting it isn’t sufficient to “not be bad.” What all skincare customers seek (natural or otherwise) are results, and as the data prove, they are willing to pay the premium for it (see Chart E).

These findings are not suggesting that brands offered in the other channels are more efficacious. Rather, it reveals the critical need to establish the perception of efficacy to gain confidence, to retain the loyalty of your most valued customers (i.e., those shopping in the food, supplement and household categories) and to give them confidence in their purchasing of HABA products in the Natural channel.

Consumer Segments of the Natural Skincare Market

The channel comparisons as shown in Charts D1–3 reveal the primary messages each retailer puts forth to their customers by virtue of the consumer purchases.

Segmentation provides a greater understanding of the market structure, characteristics and concentrations to inform opportunity.

While certain characteristics are common among the various market segments, the dominant factors for each segment are what differentiate the consumer groups and provide greater clarity about which attributes are most important. This consumer focus of the market shows where the strength of Natural Retailers provides the greatest potential to gain participation from shoppers.

The Premium Natural Skincare market clustered into five distinct segments.

• Appearance. Concerns are “looking good,” “even tone,” “large pores,” and “acne.” There is a low overall incidence of multiple skin concerns, sensitive skin and skin severity index scores.

• Aging. Concerns are “looking young,” “frown lines,” “even tone,” “pores,” “crow’s feet” and “sagging.” There is a high overall occurrence of multiple skin concerns and a low incidence of sensitive skin and skin severity index.

• Acne. The single dominant concern is “acne.” There is a high incidence of sensitive skin and skin severity index scores.

• Combination. Concerns are “looking healthy,” “combination skin” and “acne.” There is a higher incidence of multiple skin concerns and skin severity index, and a much higher incidence of sensitive skin.

• Severe. Concerns are “looking healthy.” There is a moderate index of sensitive skin and very high skin severity index scores.

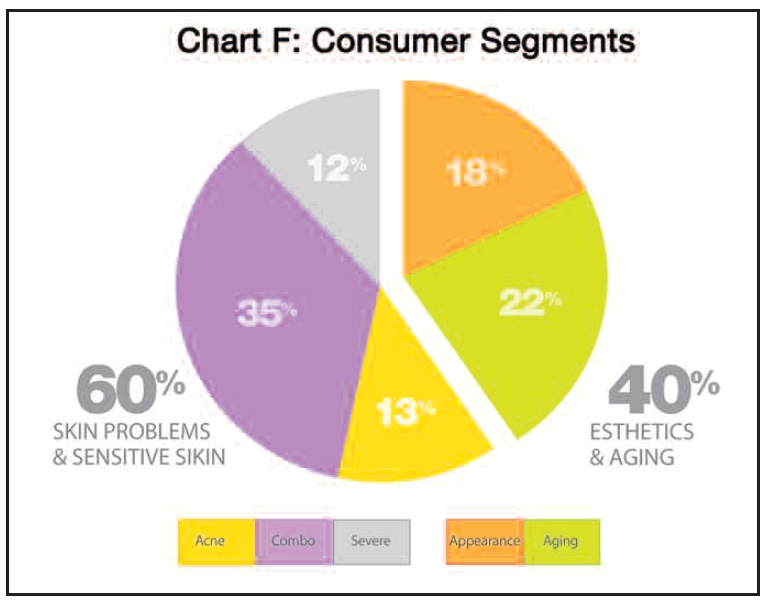

While combination skin is the largest segment followed by concerns of aging, the segments can be classified into two primary sets:

• 40% of Natural Skincare consumers focused on Esthetics and Aging.

• 60% of Natural Skincare consumers focused on Problem and Sensitive Skin.

Where anti-aging has become a dominant factor in brand offerings based on an aging population, market segmentation makes it clear that the Problem and Sensitive Skin segments dominate the natural skincare market (see Chart F).

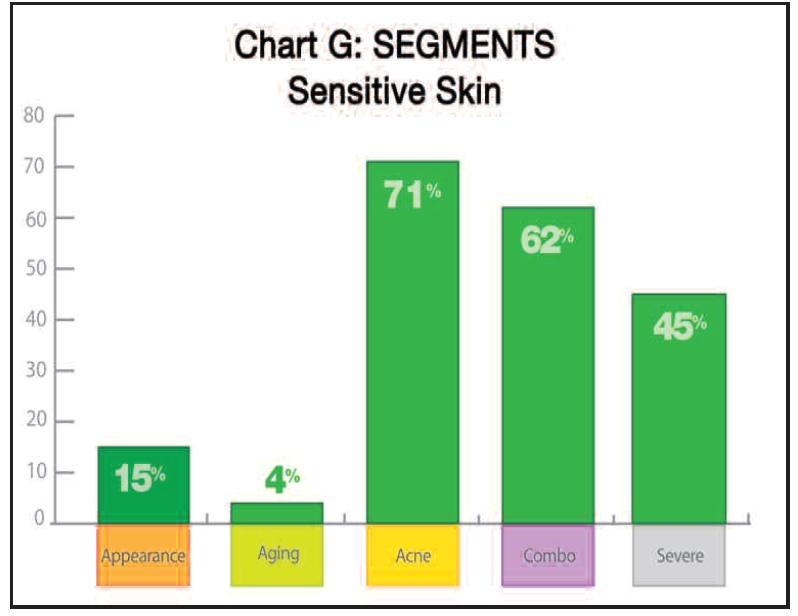

The Problem and Sensitive Skin segments have a much higher occurrence of consumers who have sensitive skin; conversely, the Appearance and Aging set has a very low occurrence of consumers who have sensitive skin (see Chart G).

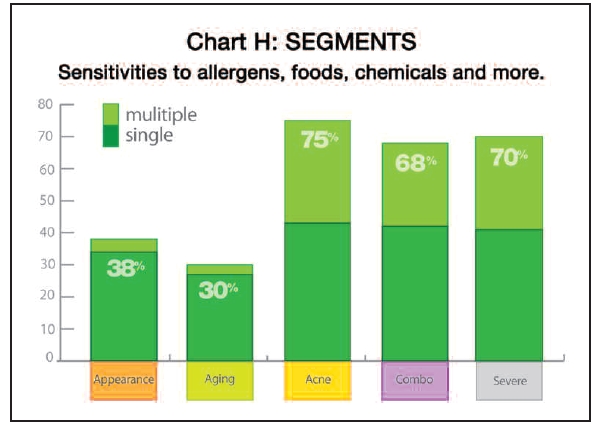

The sensitivity factor is similarly weighted. The Problem and Sensitive Skin segments strongly self-identify with food (18%), chemical (33%) and other intolerances (31%). As is often the case for people suffering from systemic imbalances, there is a high level of multiple sensitivities, as evidenced by this consumer set (see Chart H).

These consumers are highly aware and involved. Depending on the severity of their sensitivity, they are managing its implications on a daily basis. No doubt these are the lead avoidance shoppers most receptive to brands that can ensure a high level of purity and integrity, specifically avoiding any use of irritating ingredients. They may be most drawn to companies they can trust in fundamental ways.

However, the incidence of multiple skin concerns and a higher severity index (i.e., a weighting of the severity across multiple conditions) of the three segments indicate their skin problems are of greater intensity and a greater need for effective solutions.

Julia Hunter, M.D., dermatologist and founder of Wholistic Dermatology, in Beverly Hills, CA, likes to say that the skin is a window to what’s going on inside the body. “Most times sensitive skin is caused by an inflamed gut, which means you need to look at the cause of that,” she states (3).

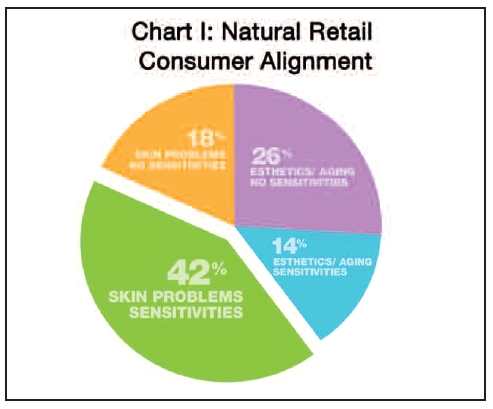

When these two factors are combined, natural skincare consumers who are managing both skin problems and sensitivities represent a significant 42% of the total Premium Natural Skincare Market (see Chart I).

When these two factors are combined, natural skincare consumers who are managing both skin problems and sensitivities represent a significant 42% of the total Premium Natural Skincare Market (see Chart I).

These are the dominant shoppers who are looking for efficacy in skincare with safety. For this, they will pay a premium, as indicated by the highest monthly spending among those in the Severe Segment.

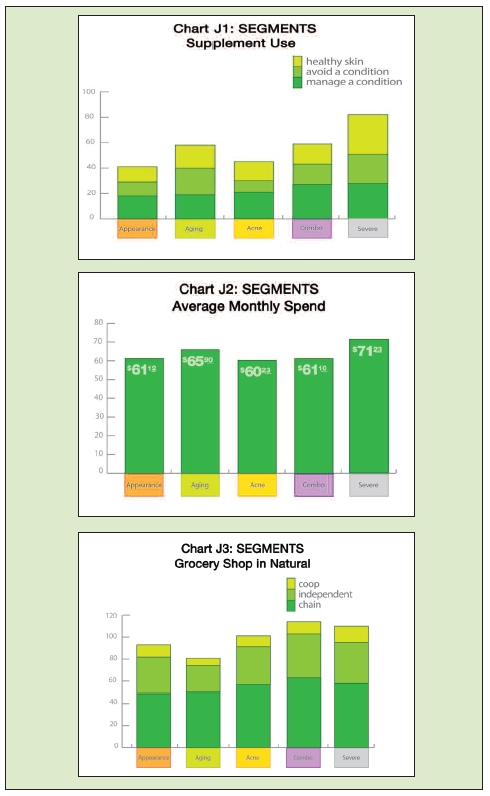

It is no coincidence that the Severe Segment also displays the highest consumption of supplements to “avoid” or “treat” a condition. Earlier research identified “condition focus” as the lead purchase motivator for the most involved supplement consumers in the natural channel. Of the Premium Natural Skincare Market, the Problem and Sensitive Skin segments display a higher frequency of shopping in Natural Retail with a high correlation of beliefs, needs and behaviors (see Charts J1–3).

A New Dialogue for Natural Retailers

It is worth repeating that the consumer who desires both efficacy and safety for their skin problems presents the greatest opportunity for Natural Retail. Note the lower significance of “gentle” as a purchase driver; “gentle” suggests lower potency and does not convey the promise of results found on other products. These consumers have greater skin challenges and are looking for the promise of efficacy.

The greatest barrier, however, to  gaining share of the high-dollar premium skincare shopper is the crisis of confidence she has with the Natural Channel as the beauty expert. The competitive channels that offer expert-assisted sales (beauty boutique, department, spa and practitioner) continually focus the conversation on results, not avoidance. Based on the established perceptions, it would be challenging to offset the confidence they enjoy using the same tactics. Natural Retailers need to establish a different position of authority for skincare to gain the consideration necessary for consumers to trust them.

gaining share of the high-dollar premium skincare shopper is the crisis of confidence she has with the Natural Channel as the beauty expert. The competitive channels that offer expert-assisted sales (beauty boutique, department, spa and practitioner) continually focus the conversation on results, not avoidance. Based on the established perceptions, it would be challenging to offset the confidence they enjoy using the same tactics. Natural Retailers need to establish a different position of authority for skincare to gain the consideration necessary for consumers to trust them.

The conversation must begin with why consumers are shopping natural and redirect the focus on how it affects their skin—specifically sensitivities and validated ingredient knowledge. This is where the Natural Retailer is the authority and can leverage cross-category, solution-based communications to raise awareness and drive traffic to the HABA section. As an example, the beauty section is just now emerging in the supplement category, which is expected to be the fastest-growing segment of supplements in the next five years, strengthening the Natural Retailers’ authority on beauty and healthy skin. And while many shoppers may understand the connection between skin health and sensitivities, many more do not. This is where the opportunity to redirect the conversation for skincare lies, and where Natural Retailers are already perceived as the authority.

Critical to this new dialogue is partnering with the right brands. Look for sophisticated premium natural skincare brands that are pure and can drive the efficacy conversation, and are willing to leverage the Natural Retailer’s strength and reinforce their authority while displaying a clear understanding of the Problem Skin and Sensitivity consumer’s needs. Natural brands can offer the level of sophistication of the competitor channels by successfully promoting efficacy through substantiated ingredient or formulation platforms with clinically proven results. The reliance on brands with the purity platform alone will not serve to reinforce the authority of Natural Retailers as a solution destination for skincare.

The 42% of the skincare market with skin problems and sensitivities is significant and the dollar share is even higher. This shopper is the premium skincare consumer, offering greater spending, more involvement and increased potential for long-term loyalty, and this consumer is already in the natural stores. WF

Kevin Williams is the principal and chief strategist of Brand Reason. A leading brand consulting and research firm dedicated to providing insight and knowledge for natural brands to find a clear path to success. For more information, visit brandREASON.com.

References

1. Packaged Facts, Natural & Organic Personal Care Products in the U.S., December 2011.

2. K. Chiarello-Ebner, “2013 WholeFoods Retailer Survey,” WholeFoods Magazine, 36 (12), 20–25 (2013).

3. “Annual Skin Care Guide,” Organic Spa Magazine, volume 8, issue 5 (2014).

Published in WholeFoods Magazine, September 2014