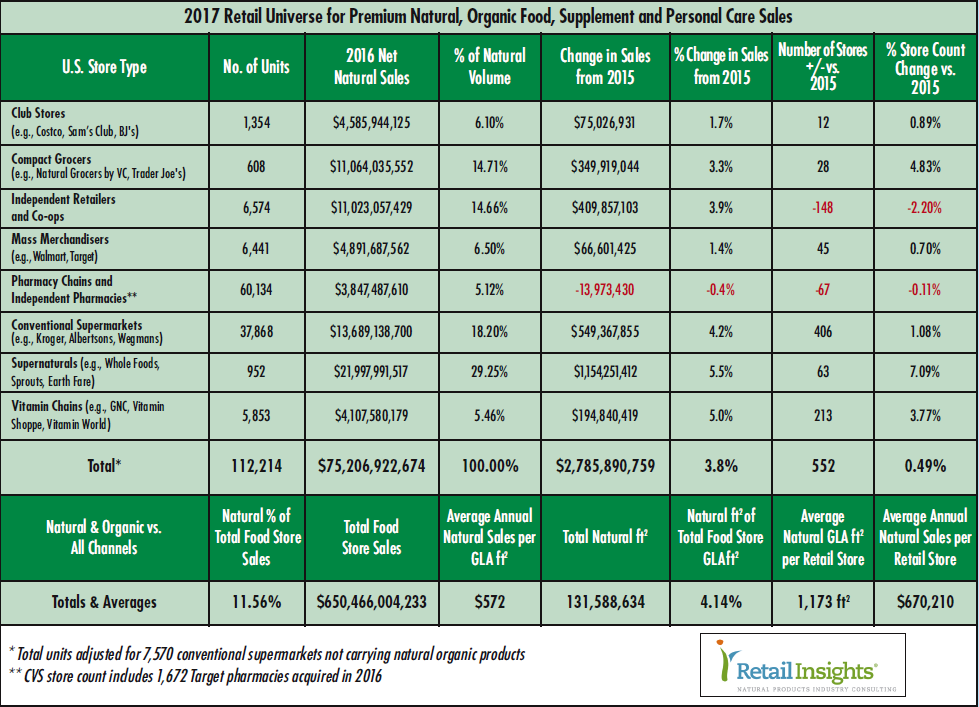

Total natural organic sales climbed $2.78 billion in 2016, or 3.8 percent, to $75.2 billion from $72.4 billion, and now account for 11.56 percent of total food store sales of $650.5 billion. The average store sells $670,210 in natural products per year, up 3.3 percent from $648,574 a year ago, and the average gross-lease-area dedicated to natural products is also up 3.7 percent, to 1,173 square feet, from 1,131 last year. Average annual sales per square foot is nearly identical, at $572 this year compared to $573 last year.

Channel AnalysisGrowth in the club store channel was subdued, with these large stores adding 2 percent to their natural square footage and gaining 1.7 in net sales, to $4.58 billion from $4.51 billion a year ago.For the compact grocer sector—stores of 20,000 square feet or less—Mrs. Greens suffered two cycles of store closings since the last analysis; currently operating just five units, down from 18 units, and a reduction in total estimated net sales of more than $50 million. Also in the compact grocer sector, Natural Grocers by Vitamin Cottage (NGVC) grew store units 25 percent, to 126 in 2016 from 101 in 2015. These younger stores led to a decline in NGVC’s average store productivity, to approximately $5.6 million per unit in 2016 compared to nearly $6.0 million last year. Rounding out the compact grocers, Trader Joe’s added 12 stores, to total 460 from 448. Overall, the compact grocer sector gained 3.3 percent in sales, to $11.06 billion from $10.7 a year ago.

For independent natural retailers and coops, a certain level of store rationalization is taking place, with a loss of 148 units, or 2.2 percent, to 6,574 stores from 6,722 stores a year ago. The surviving stores are vibrant and in growth mode, adding 6.2 percent to net sales, and averaging $1,676,766 per store compared to $1,578,875 in 2015. Average store size also increased, to 3,563 square feet per store from 3,470 a year ago. Overall, the independent channel gained 3.9 percent in net sales, to $11,023,057,429 from $10,613,200,326.

Mass merchandisers were the picture of stability, adding about 1 percent in number of units and square footage, with natural sales climbing 1.4 percent to $4.89 billion from $4.82 billion last year.

Overall, pharmacies including independents, chain stores, and in supermarkets, shed 67 stores, to 60,134 from 60,201 last year. Sales slipped 0.4 percent to $3.85 billion. For conventional supermarkets, average natural square footage per store increased 2.5 percent. The sector saw an increase in total natural sales of 4.2 percent. This is notable given the pervasive reporting of food price deflation, particularly in the fresh protein categories including dairy, beef, pork and poultry, although the natural sector may not have seen as much protein deflation.

Supernaturals are showing signs of overheating, with store counts up 7 percent, square footage up 13 percent, but total sales climbing just 5.5 percent. As a result, sector sales productivity has taken a hit, declining 6.5 percent, to $766 per square foot per year, from $819 a year ago.

Vitamin chain stores are showing discipline, growing units 3.8 percent and keeping total square footage in line with a 3.3 percent increase. Shoppers rewarded the sector, raising sales 5 percent. JJ

Published in WholeFoods Magazine January 2017

Published in WholeFoods Magazine January 2017