What is the state of the natural products industry in 2015? For a clear picture, let’s look at what the consumer wants, which has been rapidly changing.

Healthy Lifestyles

Healthy lifestyles are a growing factor in American culture, as a majority of U.S. households now actively aspire to achieve better health, and link that good health to eating good food. The desire for good nutrition will continue to drive natural and organic food sales, and also vitamin and supplement sales. Older baby boomers, those over age 65, will represent one in five Americans within the next 10–15 years. These shoppers will continue to control a multi-trillion dollar buying power, and will be happy to spend freely on preventive medicine and healthy aging.

Millennials and Gen X are also realizing they will not be able to turn back Father Time, so the clock will be ticking on their health concerns, moving them increasingly toward natural options for foods and supplements. These younger generations are also driven by the desire to raise the healthy families they are just now beginning to form, to help ensure junior gets off to a good start in life, and natural foods fit neatly into their worldview.

Better Science

At any given time, there are thousands of controlled clinical trials on nutrition going on in research centers around the world, exploring the health benefits of natural nutrients. While we are always going to see negative headlines spinning the results of nutrition studies, the good news is we are now beginning to see newer studies rebutting many of these negative findings.

As each new study bolsters the case for taking supplements, more consumers will decide to make nutritional supplementation a part of their health regime, adding to the large majority of people who already believe supplements are good for you.

Adding momentum to the better-health-through-nutrition movement is the shift in health insurance costs from employers to the employee. As each employee feels the impact of increased out-of-pocket expenses, his or her desire to control these costs increases, too. What independent natural products retailers all across the country have been reporting to me this past year is increased foot traffic and spending on preventive medicine by these same employees impacted by increased health insurance costs. It appears that, when it comes to their pocketbooks, American still believe in the adage, “An ounce of prevention is worth a pound of cure.”

The Market Responds

And food retailers have responded aggressively to the widening and deepening pool of shoppers newly interested in all things natural. The highest-profile supernaturals, including EarthFare, Fresh Thyme, Lucky’s, Sprouts Farmers Market and Whole Foods Market, all have big plans to increase the numbers of stores they operate, and are fully fueled by either private venture capital or the public markets.

In what we have been characterizing over the last several years as the “Compact Grocers,”—those stores up to about 20,000 square feet—we are seeing some of the fastest growth. Natural Grocers by Vitamin Cottage, a public company with 90 stores, plans 20% annual square-footage growth, and hopes to reach 225 stores west of the Mississippi, with the whole Eastern Seaboard yet to come in helping them achieve their stated goal of 1,100 stores.

In what we have been characterizing over the last several years as the “Compact Grocers,”—those stores up to about 20,000 square feet—we are seeing some of the fastest growth. Natural Grocers by Vitamin Cottage, a public company with 90 stores, plans 20% annual square-footage growth, and hopes to reach 225 stores west of the Mississippi, with the whole Eastern Seaboard yet to come in helping them achieve their stated goal of 1,100 stores.

Trader Joe’s—also a compact grocer—while not expanding as fast in 2014 as in previous years, still has over 400 high-volume stores with their focus on discount natural gourmet. It will be interesting to watch this space as the compact footprint lends itself to many more good-quality real estate sites than the larger 30,000 to 40,000-square-foot boxes of the supernaturals.

Everybody Wants in on the Act

Non-traditional food retailers, such as Walgreen drugstores, plan to take advantage of shoppers’ desire for foods. Along with CVS and Rite Aid, the other two major national drugstore chains, Walgreens has been adding food to its offerings. Estimates are that the drugstore channel controls 5% of all food spending.

While most of the foods these stores have been offering qualify as “convenience” items, such as milk, individual-size chilled beverages, salty snacks, candy and cookies, Walgreen has taken it one step further. With its purchase several years ago of Duane Reed, the New York City chain drugstore, Walgreen now offers fresh sushi, a large grab-and-go sandwich, wrap and salad case, and other perishables items. Walgreen wants to be the “convenience store of the future,” and it appears it was ahead of the times in betting big on fresh.

And speaking of convenience stores, operators are beginning to offer healthier fresh choices, from sandwiches and wraps to…nitrogen-flushed kombucha growler filling stations? Yes, you read that right. While not widespread yet, expect the traditional junk-food corner convenience store to continue to up their game on fresh offerings, taking their bite out of the quality food pie.

Mass Market and Club Stores

Adding to the mix is Walmart, which has introduced 100 organic food items under the Wild Oats brand in 2,000 of its 4,000 U.S. stores. Expect the number of SKUs to double as distribution reaches all 4,000 Walmart outlets over the next year or two. Of course, Walmart plans to hit a price point at least 10% lower than comparable organic products on the market now.

Costco, the powerhouse club store, continues to broaden its offering of natural and organic, with a big presence in the refrigerated, frozen and fresh-produce categories. If you are faint of heart, do not go looking for bagged washed organic salad mix; the prices will floor you.

Target is not sitting still either, retrofitting hundreds of its smaller (everything is relative) discount centers with a larger food offering, including many more SKUs of its Simply Balanced line of natural and organic private label items.

Conventional Supermarkets

We’ve seen for years the advance of mainstream supermarkets such as Kroger, Safeway, Stop & Shop, Publix and others as they expand their natural offerings, and build their own private label organic lines. Most of these stores that offer natural and organic have over 1,000 square feet of space devoted to the category, usually with many more doors of freezer and cooler than the typical independent natural products retailer.

Perhaps the most interesting recent play is the decision by Northeast regional chain Price Chopper to rebrand all its 135 stores as “Market 32,” and to completely redesign the retail space, reducing center store shelf-stable square footage, and greatly expanding all things fresh.

While other conventionals have dabbled in highlighting more fresh offerings, with a unit or two out of their larger portfolio of stores, Price Chopper is going all in with the idea of fresh across their entire enterprise. What does this tell us?

That Price Chopper realizes the fight to cut prices on center-store packaged foods is a dead end, with limited growth potential, because Americans increasingly insist on fresh food experiences that are exciting, delicious and healthy. Price Chopper and other full-line conventional supermarkets are in good position to exploit the expanding definition of “fresh,” which now includes grab-and-go, sit-down in-store dining on prepared foods, baked goods, fresh olives and marinated meats ready for cooking.

Also, with fresh, the perceived quality is higher than shelf-stable items, and the price point is higher, moving any retailer that adopts a fresh approach upmarket.

What We’ve Seen

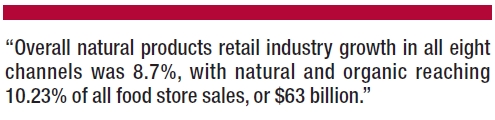

In December, as part of WholeFoods Magazine’s 37th Annual Retail Survey, my company, Retail Insights® updated our Retail Universe for Premium Natural and Organic Food, Supplement and Personal Care Sales. Overall natural products retail industry growth in all eight channels was 8.7%, with natural and organic reaching 10.23% of all food store sales, or $63 billion.

We are tracking over 110,000 stores that sell natural products, with nearly 1,500 new stores coming on stream in 2014. I firmly believe we are at the beginning of the growth curve, so hang on tight! WF

Jay Jacobowitz is president and founder of Retail Insights®, a professional consulting service for natural products retailers established in 1998, and creator of Natural Insights for Well Being®, a comprehensive marketing service designed especially for independent natural products retailers. With 38 years of wholesale and retail industry experience, Jay has assisted in developing over 1,000 successful natural products retail stores in the U.S. and abroad. Jay is a popular author, educator, and speaker, and is the merchandising editor of WholeFoods Magazine, for which he writes Merchandising Insights and Tip of the Month. Jay also serves the Natural Products Association in several capacities. He can be reached at (800)328-0855 or via e-mail at jay@retailinsights.com.

See www.wholefoodsmagazine.com/columns/merchandising-insights for additional Merchandising Insights columns.

Published in WholeFoods Magazine, January 2015